|

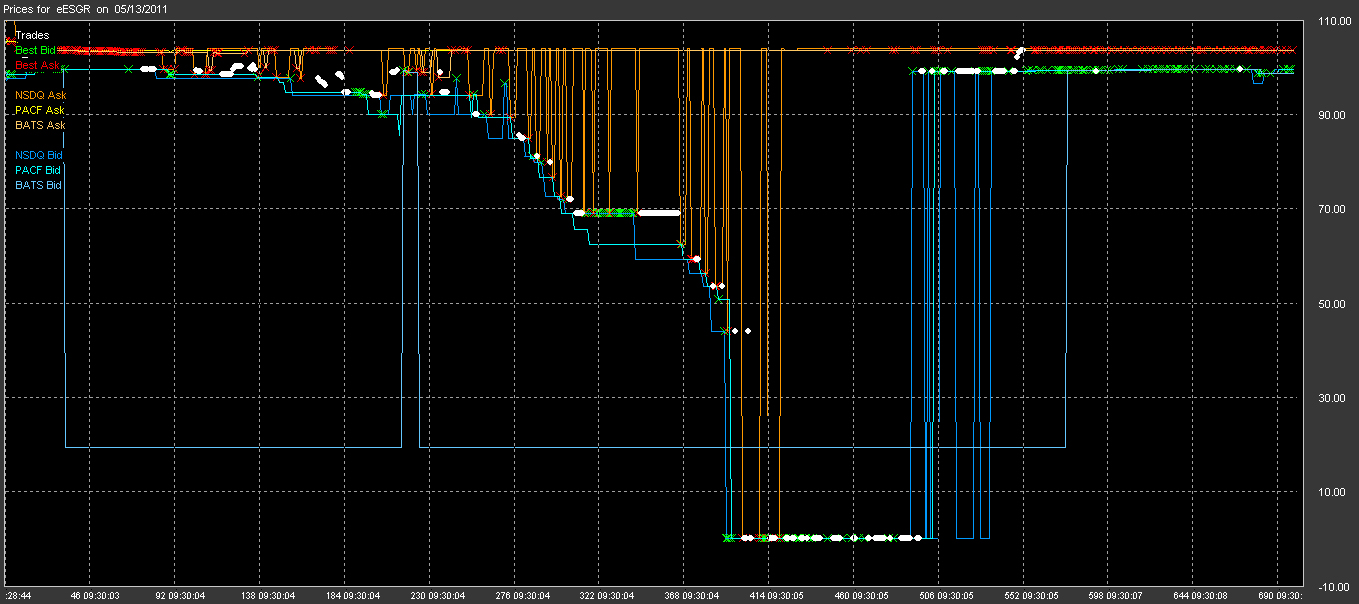

| Source: NANEX - "Equity Quote Saturation" |

CNBC mentions nothing about the money being lost to HFT or the manipulation that is costing investors purchasing power or Net Asset Value depreciation, only the loss of "confidence" and "fairness", two things that went out the window once I first saw Nanex rebuke the SEC claims. Good thing their are fines to those who manauplate the prices but who is receiving the money? The SEC for their increased Brazzers subscription? I didn't receive a check for compensation because of losses incurred in my 401 (k) from the manipulation from HFT (side note: No one else would ever mange my money, I do it all myself and if you this read this post, you'll see I've found away to work around HFT). See, we have inept regulators. These guys can't get their heads out of their asses and finally CNBC release some information that Zero Hedge, Themis Trading, & Nanex have addressed months ago and it is this, "Perhaps regulators’ biggest worry is over the unknown dynamics of the computerized stock market world that the firms are part of — and the risk that at any moment it could spin out of control". And there you have it. The regulators have no idea of the dynamics of computerized stock market trading, good thing they decided to permit it in markets before having an understanding of the dynamics it would create, f__king morons. You'll see a mention on what happened during the market close a few days ago and you can gleam some insight here. I should warn you too, you are about to here the same horse shit excuse that liquidity is added, spreads are closer and costs for trading are lower. OH REALLY!! It is this type of reporting and misinformation that makes viewers of CNBC total f__king idiots. For the most part, this network has no idea what it speaks of, except for the off chance they decided to act as the Warren Buffett PR team or in the case of Steve Liesman, the Ben Bernanke PR Team.

{kind=link}

From CNBC:

Regulators in the United States and overseas are cracking down on computerized high-speed trading that crowds today’s stock exchanges, worried that as it spreads around the globe it is making market swings worse.

The cost of these high-frequency traders, critics say, is the confidence of ordinary investors in the markets, and ultimately their belief in the fairness of the financial system.

“There is something unholy about them,” said Guy P.Wyser-Pratte, a prominent longtime Wall Street trader and investor.

“That is what caused this tremendous volatility. They make a fortune whereas the public gets so whipsawed by this trading.”

Regulators are playing catch-up. In the United States and Europe, they have recently fined traders for using computers to gain advantage over slower investors by illegally manipulating prices, and they suspect other market abuse could be going on.

Regulators are also weighing new rules for high-speed trading, with an international regulatory body to make recommendations in coming weeks.

In addition, officials in Europe, Canada and the United States are considering imposing fees aimed at limiting trading volume or paying for the cost of greater oversight.

Perhaps regulators’ biggest worry is over the unknown dynamics of the computerized stock market world that the firms are part of — and the risk that at any moment it could spin out of control.

Some regulators fear that the sudden market dive on May 6, 2010, when prices dropped by 700 points in minutes and recovered just as abruptly, was a warning of the potential problems to come.

Just last week, the broader market fell throughout Tuesday’s session before shooting up 4 percent in the last hour, raising questions on what was really behind it.

“The flash crash was a wake-up call for the market,” said Andrew Haldane, executive director of the Bank of England responsible for financial stability. “There are many questions begging.”

The industry and others say that the vast majority of trading is legitimate and that its presence means many extra buyers and sellers in the markets, drastically reducing trading costs for ordinary investors.

James Overdahl, an adviser to the firms’ trade group, said that they favor policing the market to stamp out manipulation and that they support efforts to improve market stability.

The traders, he said, “are as much interested in improving the quality of markets as anyone else.” Some academic studies show that high-frequency trading tends to reduce price volatility on normal trading days.

And while a recent analysis by The New York Times of price changes in the Standard & Poor’s 500-stock index over the past five decades showed that big price swings are more common than they used to be, analysts ascribe this to a variety of causes — including high-speed electronic trading but also high anxiety about the European crisis and the United States economy.

“We are just beginning to catch up to the reality of, ‘Hey, we are in an electronic market, what does that mean?’ ” said Adam Sussman, director of research at the Tabb Group, a markets specialist.

High-frequency trading took off in the middle of the last decade when regulatory reforms encouraged exchanges to switch from floor-based trading to electronic.

As computers took over, daily turnover of stocks rose to 8 billion shares in the United States from about 6 billion in 2007, according to BATS Global Markets.

The trading, done by independent firms or on special desks inside big Wall Street banks, now accounts for two of every three stock market trades in America.

Such trading has expanded into other markets, including futures markets in the United States.

It has also spread to stock markets around the world where for-profit exchanges are taking steps to attract their business.

When British regulators noticed strange price movements in a range of shares on the London Stock Exchange, they tracked them to a Canadian firm issuing thousands of computerized orders allegedly designed to mislead other investors.

In August, regulators fined the firm, Swift Trade, £8 million, or $13.1 million, for a technique called layering, which involves issuing and then canceling orders they never meant to carry out.

The action was challenged by Swift Trade, which was dissolved last year.

Susanne Bergsträsser, a German regulator leading a review of high-speed trading for the International Organization of Securities Commissions, said authorities have to be alert for “market abuse that may arise as a result of technological development.” The organization will present its recommendations to G-20 finance ministers this month.

In the United States, the Financial Industry Regulatory Authority last year fined Trillium Brokerage Services, a New York firm, and some of its employees $2.3 million for layering.

Even the traders’ authorized activities are coming under fire, especially their tendency to shoot off thousands of orders a second and suddenly cancel many.

Long-term investors like pension funds complain that the practice makes their trading harder.

Global regulators are considering penalizing traders if they issue but then cancel a high degree of orders, or even making them keep open their orders for a minimum time before they can cancel.

Long-term investors worry that some traders may be using their superior technology to detect when others are buying and selling and rush in ahead of them to take advantage of price moves.

Global regulators are considering penalizing traders if they issue but then cancel a high degree of orders, or even making them keep open their orders for a minimum time before they can cancel.

Long-term investors worry that some traders may be using their superior technology to detect when others are buying and selling and rush in ahead of them to take advantage of price moves.

This is driving some investors who buy and sell in large blocks to move to new so-called dark pools — venues away from public exchanges.

As more trading takes place in these venues, prices on exchanges have less meaning, critics say.

In the United States, the Securities and Exchange Commission has been looking into the new market structure for almost two years.

In July, it approved a “large trader” rule, requiring firms that do a lot of business, including high-speed traders, to offer more information about their activities in case regulators need to trace their trades.

After the flash crash, exchanges introduced circuit breakers to halt trading after violent moves.

Bart Chilton, a commissioner at the Commodity Futures Trading Commission, called for regulators to go further.

He wants compulsory registration of high-frequency firms and pre-trade testing of their algorithms.

One of the most controversial actions has been the European Commission’s recent proposal for a financial transaction tax on speculators, which would hit high-frequency firms and curtail volumes.

The proposed tax would apply to all trades in stocks, bonds and derivatives, and may face stiff opposition from European governments.

Many such firms are based in Britain or the Netherlands, and authorities fear a loss of business.

In Canada, a top regulator is proposing higher fees on the biggest players. Last year, the country put in place a monitoring system to track the 200 million to 250 million orders its exchanges receive daily — up from 70 million a year and a half ago.

And the S.E.C. last year proposed what would be an even more high-powered monitoring system called a consolidated audit trail that would gather data on trades in real time from all United States exchanges, and be a powerful tool in helping regulators piece together events in case of another flash crash.

The monitoring “will provide regulators a critical new tool to surveil the securities markets and pursue wrongdoers, in a much more efficient and effective way than we can today,” said David Shillman, associate director of the S.E.C.’s trading and markets unit.