A farce involves self-centered characters seeking to attain some type of endpoint outcome. The rumors and unfounded "chatter" driven headlines we've seen, specifically since January, have been the bullet point recap of some fantastic theater farce designed to manipulate future expectations during a period of high uncertainty and elevated market volatility.

The oil price rebound started on January 20 when Brent traded $26 handle.

Five days earlier, on January 15, Citigroup's CFO had this exchange with Mike Mayo (the analyst who was forbidden in 2002 from joining in on Citigroup conference calls):

Two days later, January 17, Zero Hedge broke a story about the Dallas Federal Reserve meeting with banks to discuss what to do with borrowers who are unable to make good on the loans they have. Zero Hedge cited a source as saying the Dallas Fed was pushing banks to seek asset sales for delinquent corporate borrowers as opposed to pushing bankruptcies.

The next day, the Dallas Fed through Twitter denied the validity of Zero Hedge's report.

One month later, February 17, The Wall Street Journal breaks the story that OPEC's President Mohammed al-Sada was going to Tehran to discuss freeze oil production at January 2016 levels. Al-Sada was to meet with leading oil Ministers from Iran, Venezuela and Iraq.

To wit:

"Qatar’s energy minister and current OPEC President Mohammed al-Sada is heading to Tehran Wednesday to discuss a plan to cap crude production with ministers from Iran, Venezuela and Iraq, people familiar with the matter said."

The timeline:

NYMEX Light Sweet contract over this time period went from $30.20 on the close February 17 to $41.75 on April 15 close. A gain for nearly 40 percent.

That’s not all. That nearly 40 percent gain meant many analysts who had bearish comments out, including recent downgrades and price target cuts, could no longer sit idle as the oil market rebounded.

- January 15 - Citi’s CFO chooses not to disclose the bank’s energy exposure on Q4 call

- January 17 - Zero Hedge breaks story of Dallas Fed pushing banks to seek asset sales from borrowers and not to push bankruptcies

- February 17 - WSJ “sources” say OPEC President to discuss freeze in Tehran - Same day FOMC Minutes for Jan. meeting are released

- February 19 - Russian 1st Dep. Minister: production freeze “could be easy”

- February 20 - Russian Dep. Minister: freeze would need to be voluntary, struggled to imagine a mechanism to control freeze

- February 22 - IEA’s Birol: Impact of Russia/Saudi freeze is limited

- February 23 - Saudi Minister: “major producers will freeze production for market to rebalance”

- March 1 - Russian Energy Min. Novak: supply should be curbed by freeze

- March 8 - Kuwait will commit to freeze if all majors plus Iran agree

- March 10 - Reuters: OPEC, NON-OPEC MEETING UNLIKELY TO HAPPEN ON MARCH 20 AS IRAN YET TO COMMIT TO OIL PRODUCTION FREEZE

- March 13 - Iranian Student News Agency says Iran will join freeze once production hits 4 million barrels per day (Mbpd)

- March 16 - Russia’s Novak: Production freeze at April Doha meeting on docket, not exports

- April 5 - Kuwait OPEC Gov: Doha agreement could freeze production at February levels or average Jan-Feb levels

- April 6 - Russia not planning to curb production on new projects, may use other measures

NYMEX Light Sweet contract over this time period went from $30.20 on the close February 17 to $41.75 on April 15 close. A gain for nearly 40 percent.

That’s not all. That nearly 40 percent gain meant many analysts who had bearish comments out, including recent downgrades and price target cuts, could no longer sit idle as the oil market rebounded.

So what do you think happened?

Those analysts now had to issue upgrades and increase price targets under the expectation that the inertia behind this recent rebound would continue.

February 25: Two days after the Saudi Minister says producers “will freeze”, Morgan Stanley initiates:

March 3: Bank of America:

March 11: Goldman Sachs updates their energy coverage:

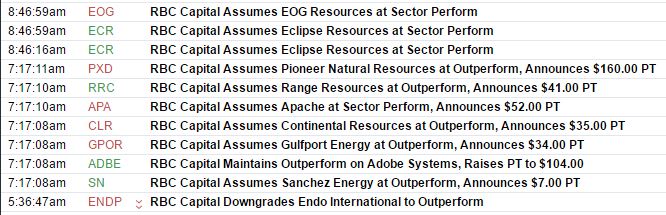

March 18: The day after Russia mentioned Doha as a meeting focused on production freeze and not on exports, Barclays & RBC updated coverage:

March 30: Seaport Global (a personal favorite) bucks the general trend by issuing a majority of downgrades:

April 1: PiperJaffray's energy focused outlet known as Simmons resumes coverage:

April 7: Nomura initiates:

You get the point. Now that we've covered January to early April, let us go back to Zero Hedge's piece about the Dallas Fed bank guidance, the very guidance the Dallas Fed openly denied it was giving. On April 3, Zero Hedge compiled two pieces, one from Bloomberg and the other from WSJ, which supported the exact claims Zero Hedge reported nearly 3 months earlier.

To wit (emphasis added):

"...when we read the Bloomberg story, we focus on this particular line: regulators - among which the Fed - "pushed lenders to focus instead on a borrower’s ability to make enough money to repay the loan, according to the person familiar with the discussions." Which sounds awfully close like "giving guidance to banks." Which, incidentally, is what the Dallas Fed tweet said it does not do when it accused us of lying. So, dear Dallas Fed, in light of today's Bloomberg article, would you like to take this chance to revise your statement which is still on the public record at the following link, and according to which you called this website liars?"

It is of no surprise that the Dallas Fed denied Zero Hedge’s now factual story that the regional Fed was offering lending guidance to banks excessively exposed to the energy sector.

It is further no surprise that a well-timed, un-sourced, and still not in writing rumor drove prices higher.

One step further, it is certainly no surprise that the price moves impacted analysts enough to review coverage, become more bullish, and subsequently drive computers and humans to buy on the new, relatively bullish.

Finally, it is no surprise there will be accountability for organizations who do things like this.

There is a war on information. The timing of a rumor is everything in the oil markets. Talk may be cheap but in oil markets it is invaluable.

What's Barry have to say now?

@DallasFed EZ template for future use:— Barry Ritholtz (@ritholtz) January 18, 2016

No truth to @zerohedge story about ___. Dallas Fed does not ___ to ___. Its a fabrication.#fail