Anytime research is released we must always be skeptic. The researchers themselves are not only worth examining but so are the sources they use. Edhec-Risk released some research they did into HFT and raise a question about the regulators and whether the "rules had changed quickly enough to keep pace with all the events in financial markets". The regulators have responded and already put restrictions in place:

- Reg-NMS: The National Market System is basically a rule set that was passed by the SEC designed to improve our exchanges by offering fair price execution processes and metrics concerning quotes, the amount, and access to market data. The ruling has four components to it (the break-down starts on page 21, last paragraph in the linked .pdf above):

- The Order Protection Rule aims to ensure that investors receive the best price when their order is executed by removing the ability to have orders traded through (executed at a worse price).

- The Access Rule, aims to improve access to quotations from trading centers in the National Market System by requiring greater linking and lower access fees.

- The Sub-Penny Rule, which sets the lowers quotation increment of all stocks over $1.00 per share to at least $0.01.

- Market Data Rules, which allocate revenue to self-regulator organizations that promote and improve market data access.

The Order Protection Rule, aka National Best Bid and Offer is a legit rule, the problem is that the SEC zeitgeist culture fails to grasp the capabilities of physicists solving light-speed problems along side the worlds best computer scientists on the street. The UK Treasury states that they found "no direct evidence" relating to the volatile price movements (for evidence read here, here, here, here, here, here, here and here). What you see in those links is more evidence that a) the SEC are narrow minded by not appreciating the abilities of people to trade at the speed of light and b) the UK Treasury does absolutely terrible research.

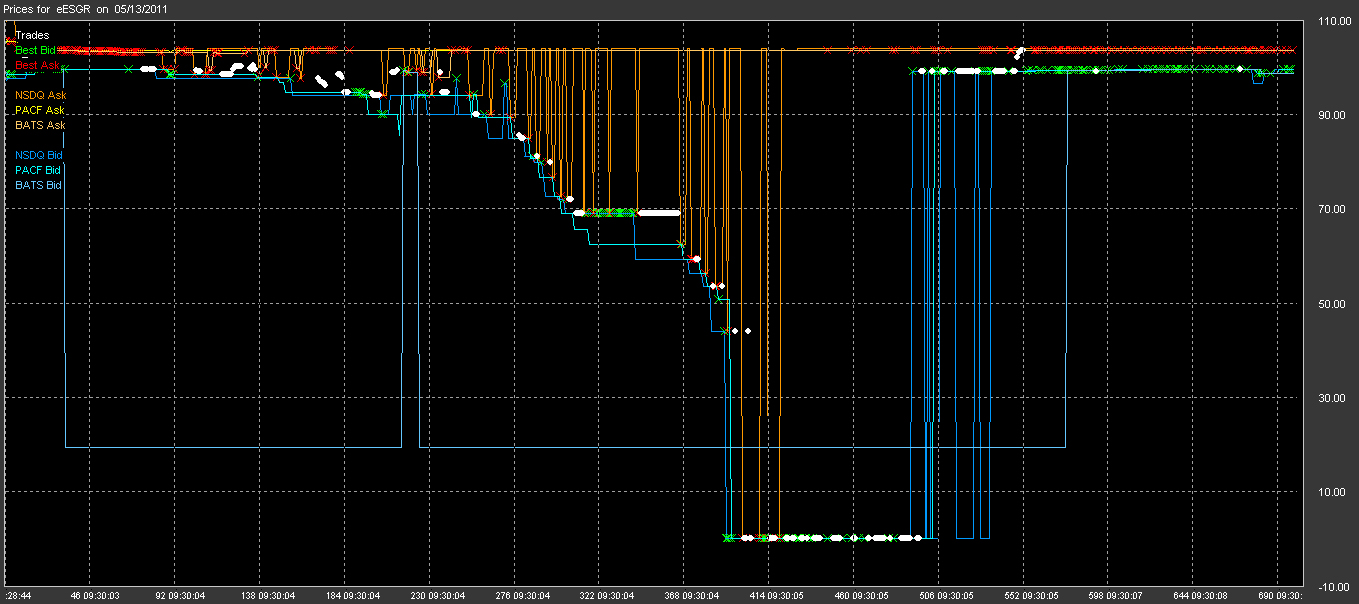

For those of you in a hurry, here are some images to debunk the premise that trades inside of a minute in a particular stock will create noise and distort the picture investigators/regulators are trying to see. And the premise that there exist "no direct evident" relating to the volatile price movements (pay attention to the X and Y Axis. Also, white dots are trades, red circles are best ask, green circles are best bid, colored lines represent exchanges):

{kind=link}

From eFinancialNews:

An influential European think-tank has released new research claiming that high-frequency trading adds to greater short-run volatility in financial markets, as the debate around the controversial activity intensifies amid greater regulatory scrutiny.

The Edhec-Risk Institute, a European centre for financial research, this week released a report on the economics of high frequency trading in which it labelled the activity as "no free lunch - if it has benefits, there must be costs."The institute, which is based in Nice in France, found that more automated trading activity is associated with "lower spreads", "more liquidity" and "better informational efficiency." However, the research also found the research also found the activity leads to "greater short-run volatility.""Our results are amazingly consistent across markets and consistent with typical HFT strategies. Short-lived orders provide liquidity when they execute and just increase volatility if they do not," the report said.The research, led by Ekkehart Boehmer, a professor of finance at the Edhec Business School, used statistical and econometric techniques to study the impact of automated and high-frequency trading across 39 markets.Boehmer concluded that "more and broader evidence" was needed to determine the impact of the activity. He also talked of the "challenges for regulators" and questioned whether "rules had changed quickly enough to keep pace with all the events in financial markets."High-frequency trading involves the use of computer-driven techniques to dip in and out of markets at sub-second speeds in order to profit from discrepancies in the price of securities across different trading venues. Firms involved in the activity have become big liquidity providers on Europe's main exchanges and account for between 50% and 70% of activity of daily European turnover in some products, according to analysts.Critics say HFT firms 'front run' institutional orders, create volatility, and damage the integrity of the markets, while defenders of the practice say it increases liquidity, narrows spreads, and reduces the overall cost of trading for investors.A number of reports around high frequency trading have been released this year, as the activity faces the threat of being shackled by new regulation including a revised version of the markets in financial instruments directive and a European financial transaction tax.Two studies commissioned by the UK Treasury last month found “no direct evidence” that HFT contributes to volatile prices.However, in October, the International Organisation of Securities Commissions, which functions as a forum for global regulators, said HFT and other high-tech trading practices "could cause market prices to move away from fundamental values in the short term and impair the price discovery process.”In November, the French senate put forward a proposal to introduce a direct tax on high-frequency trading. The proposal was the strongest and most direct policy-led attack on HFT to date, and was derided by a raft of policymakers, including Christine Lagarde, the managing director of the International Monetary Fund, and Bank of England director, Andy Haldane.One of the most senior high-frequency trading executives has come out fighting against political attacks which have threatened to shackle the industry.Speaking to Financial News last month, Remco Lenterman, managing director of Dutch HFT firm IMC and chairman of the European Principal Traders Association, the HFT lobby group launched in June, said: “The rhetoric regarding HFT has now become so fierce and the measures being proposed are so draconian that they will be immensely damaging to the marketplace and far more so than they would be to HFT firms.”